info@bazaartoday.com a property of Inrik

US Economy Outlook for the Last Week of June 2024

As we approach the end of June 2024, the US economy presents a multifaceted landscape characterized by robust GDP growth, persistent inflation, a strong labor market, evolving investment trends, and cautious Federal Reserve policies. Here’s an in-depth analysis based on the latest data and forecasts:

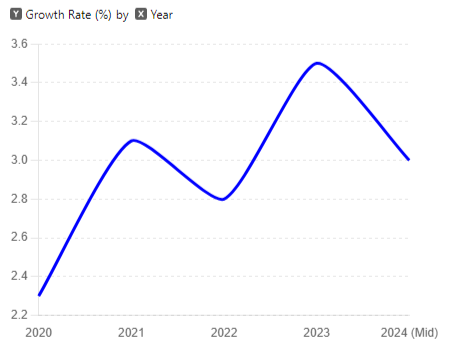

GDP Growth

The US economy continues to exhibit strong growth, with the Atlanta Federal Reserve's GDPNow model estimating a real GDP growth rate of 3.0% for the second quarter of 2024 (Atlanta Fed). This reflects a slight decline from earlier forecasts but still indicates a solid expansion driven by consumer spending and business investments. The growth momentum is expected to moderate slightly as the year progresses due to various economic headwinds.

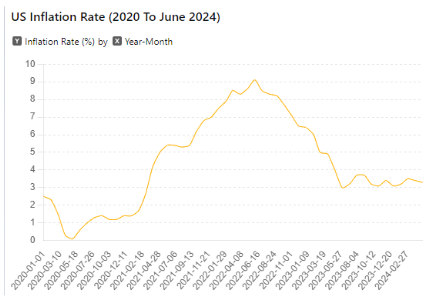

Inflation

Inflation remains a pressing concern, influenced by geopolitical conflicts and supply chain disruptions. Persistent inflation has compelled the Federal Reserve to maintain high interest rates. The inflation rate is projected to remain above 3% until mid-2025 (Deloitte United States) (J.P. Morgan | Official Website). Rising prices for imported goods, particularly oil, due to ongoing conflicts in Ukraine and the Middle East, continue to exert upward pressure on overall inflation.

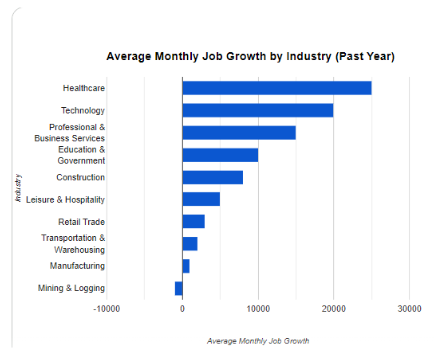

Labor Market

The labor market is a bright spot, with high employment levels and robust demand for labor. Technological advancements and increased labor force participation, including delayed retirements, have contributed to the strong labor market. However, the pace of job creation may slow down as businesses adjust to higher borrowing costs and economic uncertainties (The Conference Board) (J.P. Morgan | Official Website). The Conference Board’s Employment Trends Index also reflects these dynamics, highlighting continued but moderated job growth.

Investment

Investment activity remains resilient but cautious. Business investments, particularly in technology and infrastructure, are expected to continue growing, albeit at a slower rate due to higher interest rates. The housing sector, which has been impacted by rising mortgage rates, may see some recovery depending on future Federal Reserve policies (J.P. Morgan | Official Website).

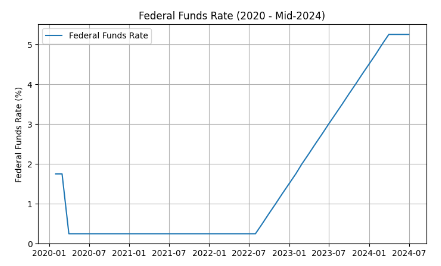

Federal Reserve and Interest Rates

The Federal Reserve has maintained a cautious stance on interest rates, focusing on combating inflation. As of now, the Fed Funds rate is expected to remain elevated at 5.25%-5.5% until mid-2024, with potential rate cuts starting in June if inflation shows signs of significant moderation (J.P. Morgan | Official Website). The Federal Reserve’s quantitative tightening program, which involves reducing its balance sheet, is expected to continue at a steady pace, removing approximately $95 billion from the economy each month throughout the year.

Conclusion

In summary, as we close out June 2024, the US economy is navigating a complex environment of robust GDP growth, persistent inflation, a strong but cautious labor market, and measured investment activity. The Federal Reserve’s policies will play a crucial role in shaping the economic landscape, with interest rate adjustments likely influencing both consumer and business behaviors in the coming months. Policymakers and market participants will need to stay alert to evolving economic indicators and global events to sustain economic stability and growth.